Tenants in Common (TIC) Investments and 1031 Exchange Considerations

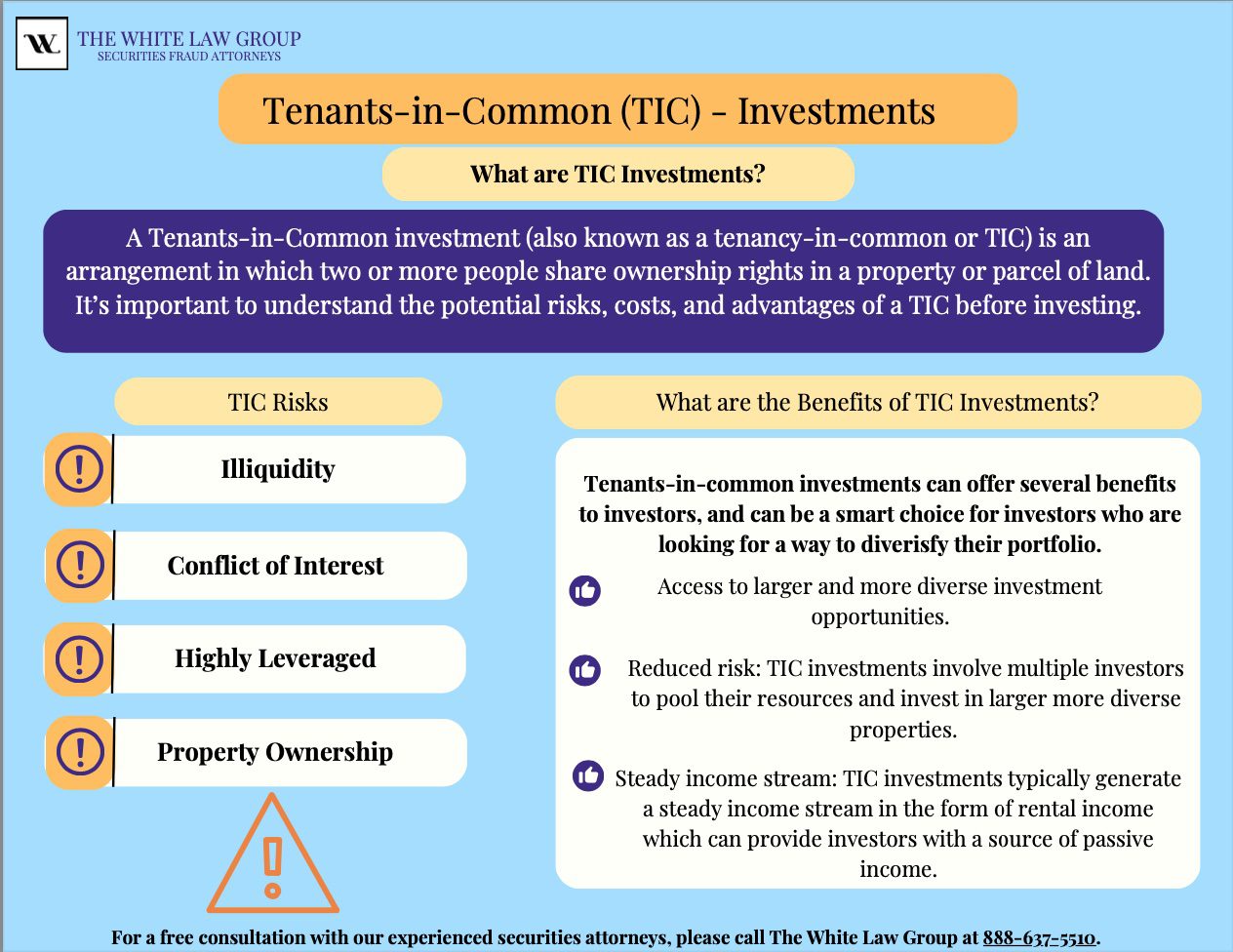

A tenants in common (TIC) investment is a real estate ownership structure where multiple investors hold fractional interests in a property. Each investor owns a direct, undivided share and participates in income, expenses, and potential appreciation.

What Is a Tenants in Common (TIC) Investment?

TIC investments are frequently used in 1031 exchanges, which allow investors to defer capital gains taxes by reinvesting into qualifying real estate. Because of this, you may also hear them referred to as 1031 TIC investments.

These investments are often marketed as:

- Passive income opportunities

- Access to institutional-quality real estate

- Tax-advantaged 1031 exchange solutions

However, what appears straightforward on the surface can become significantly more complex in practice. TIC structures involve multiple owners, layered entities, and long-term commitments that can be difficult to exit.

How Do 1031 TIC Investments Work?

In a typical 1031 TIC investment:

- A sponsor acquires a commercial property

- Ownership is divided into fractional interests

- Interests are sold to investors, often at a markup

- Investors hold title directly as tenants in common

- A management entity operates the property

Because investors hold direct ownership in real estate, TICs may qualify under IRS rules for a 1031 like-kind exchange, allowing tax deferral on capital gains.

Income is distributed to investors after expenses, but performance depends heavily on the sponsor, property management, and market conditions.

TIC vs. DST: Key Differences in 1031 Exchange Investments

Investors often compare TIC vs. DST structures when evaluating 1031 exchange options.

Key differences include:

- Ownership Structure:

TIC investors own a direct interest in real estate

DST investors own a beneficial interest in a trust - Decision-Making:

TICs may require coordination among multiple owners

DSTs centralize control under a trustee - Liability Protection:

TIC structures may expose investors to greater liability

DSTs generally provide limited liability protection - Operational Complexity:

TICs tend to be more complex to manage

DSTs are more passive but still carry risk

While 1031 DSTs have gained popularity in recent years, both TIC and DST investments involve significant risks that investors should fully understand.

Why Brokers Recommend Tenants in Common Investments

Brokerage firms often promote TIC investments based on several perceived benefits:

- Capital gains tax deferral through a 1031 exchange

- Passive income potential

- Access to larger commercial assets

However, TIC investments also typically pay high commissions to financial advisors—often 7% or more. This can create a conflict of interest, particularly if the investment is not suitable for the client.

Risks of Tenants in Common (TIC) Investments

The risks of tenants in common investments are substantial and often understated—particularly in the context of 1031 TIC investments, where tax benefits may overshadow investment fundamentals.

Illiquidity

TIC investments are typically long-term and illiquid. Investors may not be able to sell their interest without approval from other owners or until the property is sold.

Shared Control and Decision-Making

Some TIC structures require unanimous or majority consent for key decisions such as selling or refinancing, which can create delays or disputes.

Sponsor and Management Risk

Investors rely heavily on the sponsor and property manager. Poor performance or conflicts of interest can negatively impact returns.

High Fees and Commissions

TIC investments often include high upfront commissions (commonly 5–10%), which can reduce overall profitability.

Leverage Risk

Many TIC properties use significant debt. Even small market changes can increase the risk of default.

Suitability Concerns

These investments are sometimes recommended to conservative or retired investors seeking income, despite their complexity and illiquidity.

Why TIC Investments Are Used in 1031 Exchanges

The primary appeal of a 1031 TIC investment is the ability to defer capital gains taxes.

Under IRS Section 1031:

- Investors can reinvest proceeds from the sale of investment property

- Taxes on gains are deferred (not eliminated)

- Replacement property must meet like-kind requirements

However, investors should carefully weigh:

- Liquidity constraints

- Long-term investment risk

- Dependence on sponsor performance

Focusing solely on tax deferral can lead to overlooking key risks.

Common TIC and 1031 Investment Sponsors

TIC sponsors source, structure, and manage these investments, typically earning fees through markups and ongoing management.

Examples of TIC and DST sponsors include:

- Inland Real Estate

- Cabot Investment Properties

- Cottonwood Residential

- Griffin Capital

- Avistone Commercial Real Estate

- Madison Capital Group

Sponsor quality and incentives can significantly impact investment outcomes, making due diligence critical.

Frequently Asked Questions

What is a 1031 TIC investment?

A 1031 TIC investment is a tenants in common structure used in a 1031 exchange, allowing investors to defer capital gains taxes by purchasing fractional ownership in real estate.

Are tenants in common investments suitable for all investors?

No. TIC investments are generally illiquid and complex. Financial advisors should evaluate suitability based on an investor’s risk tolerance, time horizon, and liquidity needs.

What is the difference between TIC and joint tenancy?

In a TIC, each owner holds a separate, transferable interest. Joint tenancy typically includes rights of survivorship, meaning ownership passes automatically to other owners.

Can you lose money in a TIC investment?

Yes. TIC investments carry risks including market downturns, leverage, and management issues, all of which can result in losses.

What is FINRA arbitration?

FINRA arbitration is a dispute resolution process used to resolve claims between investors and brokerage firms, often involving allegations of unsuitable investment recommendations or misrepresentation.

Recovering Losses from TIC Investments

If you suffered losses in a tenants in common (TIC) or DST investment due to misrepresentation, unsuitable recommendations, or inadequate due diligence, you may have legal options.

The securities attorneys at The White Law Group represent investors nationwide in FINRA arbitration claims involving complex investments, including 1031 TIC investments.

Contact us for a free consultation at 888-637-5510.