Broker Churning: How to Spot Excessive Trading and Recover Investment Losses

If you believe your broker engaged in excessive trading or churned your account, you may be entitled to financial recovery.

Table of Contents

ToggleRecovering Investment Losses from Broker Churning

Broker churning is a form of securities fraud in which a financial advisor excessively trades securities in a client’s account to generate commissions—often at the investor’s expense. If you suffered losses due to excessive trading, the attorneys at The White Law Group may be able to help you recover through FINRA arbitration.

This page is part of our Types of Investment Fraud resource center, where we explain common forms of broker misconduct and investor recovery options.

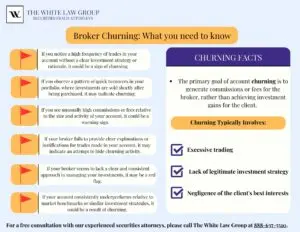

What Is Broker Churning?

Broker churning occurs when a broker places frequent buy and sell trades in a customer’s account without a legitimate investment purpose, primarily to generate commissions or fees.

This misconduct typically involves:

- Excessive trading activity inconsistent with your investment goals

- Lack of a reasonable investment strategy

- Disregard for your financial objectives and risk tolerance

- High commissions and transaction costs that erode returns

Churning is a violation of industry rules enforced by the Financial Industry Regulatory Authority (FINRA) and may also violate federal securities laws.

Common Examples of Broker Churning

Broker churning can take several forms, including:

- Excessive Trading: Frequent, unnecessary trades that generate commissions

- Unauthorized Trading: Trades placed without your approval

- Frequent Switching: Moving assets between investments without justification

- Unsuitable Recommendations: Encouraging trades that don’t fit your profile

- Ignoring Investment Objectives: Disregarding your stated goals

- Failure to Diversify: Concentrating assets while continuing to trade excessively

Red Flags of Investment Churning

You may be a victim of broker churning if you notice:

- High trading volume with no clear strategy

- Rapid buying and selling of the same securities

- Excessive commissions relative to account size

- Transactions you did not authorize

- Poor performance despite active trading

- Lack of clear explanations from your broker

While active trading can be legitimate in some cases, patterns of excessive activity combined with losses often signal misconduct.

How to Prove a Broker Churning Claim

To recover losses, investors typically must prove three key elements in FINRA arbitration:

1. Control of the Account

The broker exercised control over trading decisions, either:

- Through discretionary authority, or

- By the investor consistently relying on the broker’s recommendations

2. Excessive Trading

Trading activity was excessive in light of your investment objectives.

Two common metrics include:

- Turnover Ratio:

- 2 = potentially excessive

- 4 = presumptively excessive

- 6+ = strong evidence of churning

- Cost-to-Equity Ratio (C/E Ratio):

Measures how much your account must earn just to break even after fees

3. Scienter (Intent)

The broker acted with intent to defraud or reckless disregard for your interests.

FINRA Rules Related to Churning

Churning claims are often based on violations of FINRA Rule 2111 (Suitability), which requires brokers to ensure that investment strategies are appropriate for the client.

Excessive trading can violate quantitative suitability, even if individual trades appear suitable on their own.

Recovering Losses Through FINRA Arbitration

Most brokerage agreements require disputes to be resolved through FINRA arbitration, not court litigation.

The process generally includes:

- Filing a Statement of Claim

- Selection of a panel of arbitrators

- Exchange of documents and evidence

- Arbitration hearing

- Binding decision (award)

Investors may be able to recover:

- Excessive commissions and fees

- Portfolio losses

- Lost opportunity damages

- Interest and costs

Common Defenses Used by Brokerage Firms

Brokerage firms often defend churning claims by arguing:

“The Client Controlled the Account”

They may claim you approved or directed trades.

“You Accepted the Trades”

Firms may argue:

- You received trade confirmations

- You failed to object in time

However, arbitration panels often recognize that confirmation statements alone do not prove informed consent.

Documents Needed for a Churning Claim

To evaluate your case, attorneys typically review:

- Account statements

- Trade confirmations

- New account forms and agreements

- Commission and compensation records

- Correspondence with your broker

These documents help establish excessive trading and broker incentives.

Why Broker Churning Matters

Even if individual trades seem small, the cumulative effect of excessive commissions and poor strategy can significantly damage a portfolio over time.

Churning is particularly harmful to:

- Retirees and conservative investors

- Individuals relying on income or preservation strategies

• Investors who trusted their advisor’s recommendations

Speak with a Broker Churning Attorney

If you believe your broker engaged in excessive trading or churned your account, you may be entitled to financial recovery.

The White Law Group represents investors nationwide in claims involving:

- Broker churning

- Unauthorized trading

- Unsuitable investments

- Selling away

- Other forms of securities fraud

With offices in Chicago and Seattle, our FINRA arbitration attorneys represent investors in all 50 states. For a free consultation, call (888)637-5510.

Frequently Asked Questions

What is the difference between active trading and churning?

Active trading can be legitimate if it aligns with your goals. Churning occurs when trading is excessive and primarily benefits the broker.

What is a turnover ratio in churning cases?

It measures how frequently securities are bought and sold relative to account value. High ratios may indicate excessive trading.

Can I recover losses from broker churning?

Yes. Investors may recover losses through FINRA arbitration if misconduct is proven.

How long do I have to file a claim?

FINRA typically requires claims to be filed within six years of the misconduct, but there are exceptions.