What Is FINRA Rule 2111 Suitability?

FINRA Rule 2111, commonly known as the suitability rule, requires brokers and brokerage firms to recommend only investments that are appropriate for their clients based on their financial situation and investment objectives.

This rule is a key investor protection designed to prevent unsuitable investment recommendations.

What Does the Suitability Rule Require?

Under FINRA Rule 2111, brokers must have a reasonable basis to believe that a recommendation is suitable based on the investor’s profile, including:

- Financial situation

- Investment objectives

- Risk tolerance

- Investment experience

- Time horizon

- Liquidity needs

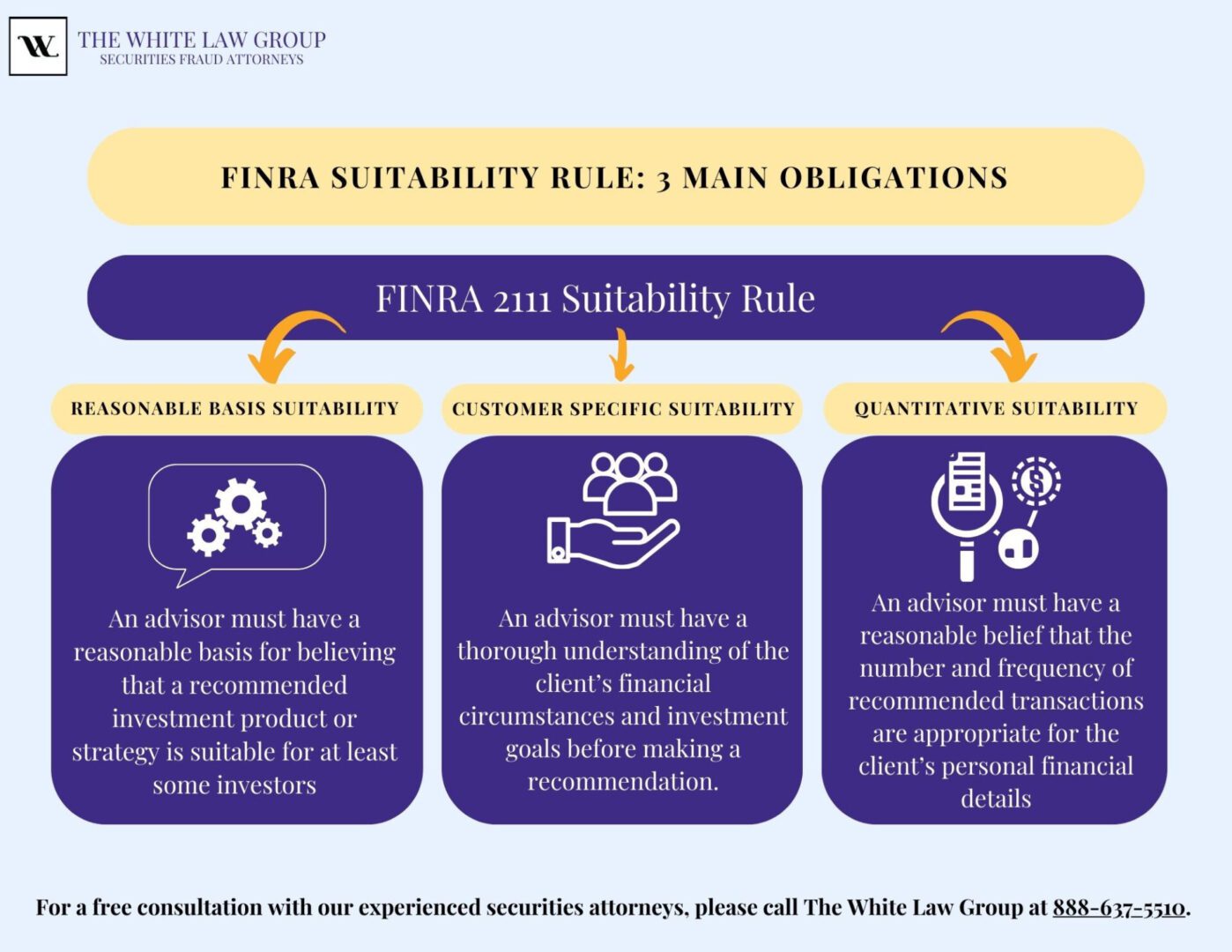

The Three Suitability Obligations

Reasonable Basis Suitability

Brokers must understand the risks and features of an investment before recommending it.

Customer-Specific Suitability

Recommendations must align with the individual investor’s financial profile and goals.

Quantitative Suitability

The overall pattern of trading must not be excessive or inconsistent with the investor’s best interests.

Your Investment Profile and Why It’s Important

An investment profile is the information brokers collect to determine suitability, including:

- Age

- Income and net worth

- Investment objectives

- Risk tolerance

- Liquidity needs

- Tax status

Examples of Suitability Violations

- Recommending high-risk investments to conservative investors

- Overconcentration in a single asset

- Excessive trading (churning)

- Recommending complex products without proper explanation

When Does a Suitability Violation Become a Legal Claim?

Not every unsuitable recommendation results in a claim, but when investors suffer losses due to violations of FINRA Rule 2111, they may have legal options.

Learn more about your rights and recovery options by visiting our Unsuitable Investment Lawyer page.

Broker Misconduct and Liability

Brokerage firms may be held liable for failing to supervise advisors or allowing unsuitable recommendations.

Investors may pursue claims through FINRA arbitration to recover investment losses.