Unsuitable Investment Lawyer – FINRA Rule 2111 Suitability Violations

Unsuitable investments occur when a broker or financial advisor recommends investments that are inconsistent with an investor’s financial situation, investment objectives, or risk tolerance. When financial professionals fail to properly evaluate a client’s needs before recommending securities, those recommendations may violate industry rules and expose investors to unnecessary risk.

Table of Contents

ToggleThe Financial Industry Regulatory Authority (FINRA) regulates brokerage firms and financial advisors in the United States. FINRA rules require brokers to recommend only investments that are appropriate for their clients. When brokers violate these obligations, investors may have the right to pursue claims to recover investment losses.

If you believe a broker recommended unsuitable investments that resulted in financial losses, an experienced unsuitable investment lawyer can evaluate whether misconduct occurred and whether you may be able to recover losses through FINRA arbitration.

FINRA Rule 2111 – The Suitability Rule

FINRA Rule 2111, commonly referred to as the Suitability Rule, requires brokerage firms and financial advisors to have a reasonable basis for believing that an investment recommendation is suitable for the customer.

The rule requires brokers to evaluate a customer’s investment profile before making recommendations. According to FINRA, an investor’s profile may include:

- Age

- Other investments

- Financial situation and needs

- Tax status

- Investment objectives

- Investment experience

- Investment time horizon

- Liquidity needs

- Risk tolerance

Brokers must have a thorough understanding of both the investment product and the customer’s financial profile before making recommendations. When brokers fail to conduct appropriate due diligence or recommend investments that do not match an investor’s profile, they may violate FINRA Rule 2111.

Brokerage firms that fail to supervise brokers or allow unsuitable recommendations may also be held responsible for investor losses through FINRA arbitration claims.

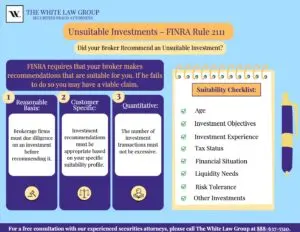

The Three Suitability Obligations Under FINRA Rule 2111

FINRA Rule 2111 identifies three core suitability obligations that securities attorneys often analyze when evaluating unsuitable investment claims.

Reasonable Basis Suitability

A broker must have a reasonable basis to believe that an investment recommendation is suitable for at least some investors. This requires the broker to perform adequate due diligence and fully understand the risks, features, and potential performance of the recommended investment.

If a broker recommends a product they do not fully understand or fails to investigate its risks, the recommendation may violate the suitability rule.

Customer-Specific Suitability

Customer-specific suitability requires brokers to determine whether an investment is suitable for a particular investorbased on their financial circumstances and investment goals.

Factors brokers must consider include:

- retirement plans

- investment experience

- financial resources

- risk tolerance

- liquidity needs

- time horizon

Many unsuitable investment cases arise when brokers recommend investments that are inconsistent with a client’s risk tolerance or financial goals.

Quantitative Suitability

Quantitative suitability focuses on whether a broker recommended too many transactions within a client’s account.

Even if individual investments may be suitable, the overall trading activity may be excessive. Excessive trading — commonly referred to as churning — may generate commissions for brokers while harming the investor.

What Is an Investor Suitability Profile?

Before recommending investments, brokers must collect information about a client’s investment profile. This information helps determine whether investment recommendations are appropriate.

Important components of an investor profile include the following:

Age of the Investor

An investor’s age may significantly influence the suitability of an investment strategy. Younger investors may have a longer time horizon and may tolerate higher levels of risk. Investors approaching retirement often require more conservative strategies focused on capital preservation.

Investment Objectives

When opening a brokerage account, investors typically select investment objectives such as:

- capital preservation

- income generation

- growth and income

- capital appreciation

- aggressive growth

Investment recommendations should align with these stated objectives. Recommending high-risk investments to investors seeking capital preservation may constitute unsuitable investment advice.

Other Investments and Diversification

Financial advisors must consider a client’s existing investments before recommending additional securities. Proper diversification may reduce portfolio risk by spreading investments across multiple asset classes.

Overconcentrating an investor’s portfolio in one security or sector may increase risk and may be considered an unsuitable recommendation.

Tax Status

Investment recommendations may also carry tax implications. Certain transactions, such as switching variable annuities or selling long-term investments prematurely, may trigger unnecessary tax consequences for investors.

A broker who fails to consider tax implications when recommending investments may be exposing a client to avoidable losses.

Financial Situation and Needs

Brokers must consider a client’s financial resources, including income, assets, liabilities, and financial obligations. Investment recommendations should reflect the investor’s ability to withstand potential losses.

Investment Experience

Certain securities may only be appropriate for sophisticated investors. Complex or speculative investments may be unsuitable for investors who lack the experience necessary to understand the associated risks.

Liquidity Needs

Some investments are difficult to sell quickly. Illiquid investments — such as private placements or non-traded REITs— may be unsuitable for investors who may need access to their funds in the near future.

Risk Tolerance

Risk tolerance is one of the most important factors in determining investment suitability. Brokers must ensure that investment recommendations match the investor’s willingness and ability to tolerate losses.

Common Examples of Unsuitable Investment Recommendations

The following situations may indicate that a broker recommended unsuitable investments:

High-Risk Investments for Conservative Investors

If a broker recommends speculative investments to a conservative investor seeking stability, the recommendation may violate FINRA suitability rules.

Lack of Diversification

Placing a large portion of a client’s portfolio into a single security or narrow sector can expose investors to significant risk.

Illiquid Investments

Investments with limited liquidity, such as private placements or non-traded real estate investment trusts, may be unsuitable for investors who require access to their funds.

Complex Investment Products

Structured products, derivatives, or alternative investments may carry risks that some investors may not fully understand.

Excessive Trading (Churning)

Churning or frequent trading in an account primarily to generate commissions may violate suitability rules and harm investor returns.

Recovering Losses Through FINRA Arbitration

Most disputes between investors and brokerage firms are resolved through FINRA arbitration, a dispute resolution process administered by the Financial Industry Regulatory Authority.

When investors open brokerage accounts, they typically sign agreements requiring disputes to be resolved through arbitration rather than court litigation.

To begin the process, investors file a Statement of Claim with FINRA describing the misconduct and the financial losses suffered. Arbitrators then review evidence, hear testimony, and issue a binding decision known as an arbitration award.

FINRA arbitration may allow investors to recover compensation for losses caused by unsuitable investment recommendations.

Contact an Unsuitable Investment Lawyer

If you believe a broker recommended unsuitable investments that resulted in financial losses, the attorneys at The White Law Group may be able to help.

Our securities fraud attorneys represent investors nationwide in claims against brokerage firms involving many types of investment fraud:

- unsuitable investments

- broker misrepresentations

- unauthorized trading

- churning

- selling away

- securities fraud

The White Law Group is a national securities arbitration and investor protection law firm with offices in Chicago and Seattle. Since the firm launched in 2010, it has handled hundreds of FINRA arbitration cases on behalf of investors.

If you believe you have suffered losses due to unsuitable investments, contact The White Law Group for a free consultation at (888) 637-5510.

Frequently Asked Questions

Brokers have a fiduciary duty to act in their clients’ best interest and must adhere to FINRA’s “suitability rule” (Rule 2111). This rule requires brokers to:

- Understand the client’s financial profile.

- Recommend investments that match the client’s goals and risk tolerance.

- Avoid high-risk investments for clients seeking conservative growth or income.

An investment may be unsuitable if:

- It involves risks the client was unaware of or did not consent to.

- The investment does not match the client’s financial needs, such as liquidity requirements or time horizon.

- It results in excessive losses or costs due to high fees or frequent trading.

Common examples include:

- High-risk investments like penny stocks or leveraged ETFs for conservative investors.

- Illiquid investments, such as private placements or non-traded REITs, for investors needing quick access to funds.

- Over-concentration in a single security, sector, or asset class.

- Recommendations of complex or high-risk securities you do not understand.

- High-pressure sales tactics or frequent trading in your account (churning).

- Losses that are inconsistent with your risk tolerance or financial goals.