Margin Trading Losses & Margin Account Fraud – Investor Claims

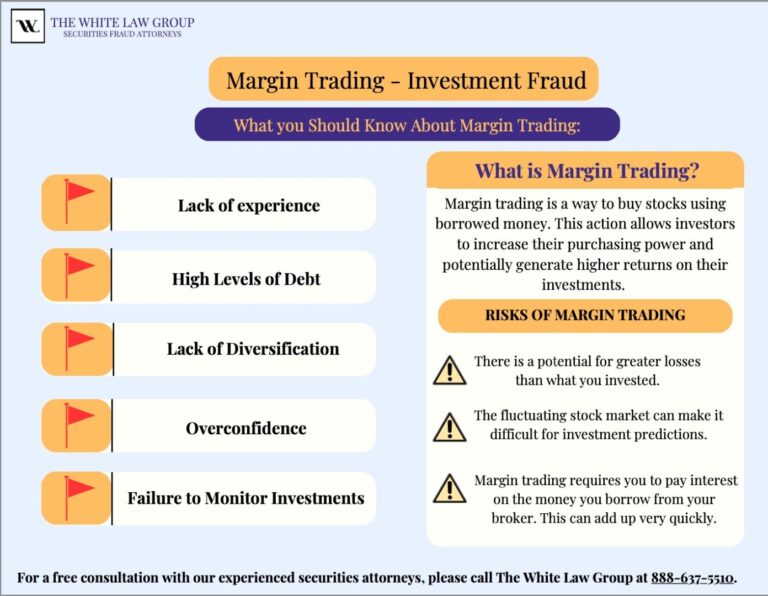

Margin trading allows investors to borrow money from a brokerage firm to purchase securities. While margin accounts can increase an investor’s purchasing power, they also significantly increase risk. If investments decline in value, investors may lose more than their initial investment and may be required to deposit additional funds to maintain the account.

Table of Contents

ToggleIn some cases, brokers recommend or use margin trading in ways that are unsuitable for the investor’s financial situation, risk tolerance, or investment objectives. When brokers fail to properly explain the risks or encourage excessive leverage in an account, investors may suffer substantial losses.

Recovery of Margin Trading Losses

The securities fraud attorneys at The White Law Group represent investors nationwide in claims involving margin trading losses, unsuitable margin recommendations, and brokerage firm misconduct.

What Is Margin Trading?

Margin trading involves borrowing money from a broker-dealer to purchase securities such as stocks or other investments. The securities purchased serve as collateral for the loan.

When you open a margin account, you deposit a portion of the purchase price of the securities, known as the initial margin. Under industry rules, investors generally must deposit at least 50% of the purchase price, while the broker provides the remaining funds.

While margin trading can amplify gains, it also magnifies losses. If the value of the securities declines, investors may be required to deposit additional funds or sell investments at a loss.

Because of these risks, margin trading may be inappropriate for many investors, particularly those seeking capital preservation or lower-risk investment strategies.

Broker Misconduct Involving Margin Accounts

Margin accounts are subject to strict regulatory requirements, but misconduct can still occur. Brokers and brokerage firms have a duty to recommend investments and strategies that are suitable for their clients.

Common forms of misconduct involving margin accounts include:

- Recommending margin trading to conservative or inexperienced investors

- Failing to explain the risks associated with margin trading

- Using margin to increase commissions through excessive trading or churning

- Allowing excessive leverage in an account

- Using margin without proper authorization

- Failing to properly supervise margin activity in customer accounts

When brokers misuse margin accounts or recommend margin trading strategies that are unsuitable, investors may have grounds to pursue financial recovery through arbitration.

Risks of Margin Trading

Margin trading can significantly increase investment risk. Investors should fully understand the potential consequences before trading on margin.

Key risks include:

Magnified Losses

Because margin trading involves borrowed funds, losses can exceed the investor’s original investment.

Margin Calls

If the value of the securities in a margin account falls below required levels, the brokerage firm may issue a margin call requiring the investor to deposit additional funds.

Forced Liquidation

If an investor cannot meet a margin call, the brokerage firm may sell securities in the account without prior notice to cover the loan.

Interest Costs

Investors who borrow funds to purchase securities must pay interest on the margin loan, which can increase losses if investments decline.

Market Volatility

Rapid market fluctuations can trigger margin calls and forced sales during unfavorable market conditions.

Maintenance Margin Requirements

Margin accounts must maintain a minimum level of equity known as the maintenance margin. Most brokerage firms require investors to maintain between 30% and 40% equity in their margin accounts.

If the equity in an account falls below the maintenance requirement, the brokerage firm may issue a margin call demanding additional funds or securities.

Investors who fail to meet a margin call risk having securities sold by the firm to restore the required margin levels. In many cases, brokerage firms may liquidate positions without consulting the investor.

FINRA Rule 4210 and Margin Requirements

Margin trading is regulated by FINRA Rule 4210, which establishes margin requirements for broker-dealers and their customers.

FINRA created Rule 4210 to help manage risk within the securities industry and limit excessive leverage in investor accounts. The rule requires brokerage firms to collect and maintain minimum margin levels when customers engage in certain securities transactions.

The rule also outlines requirements for:

- Calculating margin levels

- Maintaining sufficient collateral in margin accounts

- Monitoring risk exposure related to margin trading

These requirements are designed to promote responsible risk management by brokerage firms and help maintain stability in the financial markets.

When Margin Trading Becomes Unsuitable

Margin trading is not appropriate for every investor. In many cases, the strategy may be unsuitable for individuals with conservative investment goals or limited financial resources.

Margin trading may be unsuitable when:

- The investor has a low risk tolerance

- The investor is retired or nearing retirement

- The investor relies on investments for income

- The investor lacks experience with complex investment strategies

Brokers who recommend margin trading without properly evaluating a client’s financial situation or explaining the risks may violate industry rules.

Recovering Margin Trading Losses Through FINRA Arbitration

Many brokerage account agreements require disputes between investors and brokerage firms to be resolved through FINRA arbitration rather than in court.

FINRA arbitration allows investors to pursue claims against brokerage firms for misconduct such as:

- Unsuitable margin recommendations

- Failure to disclose margin risks

- Unauthorized margin trading

- Failure to supervise margin activity

The White Law Group represents investors nationwide in FINRA arbitration claims involving margin account losses and brokerage misconduct.

Free Consultation

If you suffered significant losses related to margin trading or believe your broker improperly recommended margin strategies, you may have legal options.

The White Law Group is a national securities fraud and investor protection law firm representing investors in claims against brokerage firms and financial professionals across the United States.

Since its founding, the firm has handled hundreds of FINRA arbitration cases involving broker misconduct and investment fraud losses.

The White Law Group has offices in Chicago, Illinois and Seattle, Washington, and represents investors in all 50 states.

For a free consultation with a securities fraud attorney, please contact The White Law Group at 888-637-5510.

Frequently Asked Questions

Margin trading allows investors to borrow money from a brokerage firm to purchase securities. While this increases buying power, it also increases potential losses because investors are using borrowed funds.

A margin call occurs when the value of securities in a margin account falls below the required maintenance margin. The brokerage firm may require the investor to deposit additional funds or securities to maintain the account.

Investors may be able to recover losses if their broker recommended unsuitable margin strategies, failed to explain the risks, or engaged in misconduct involving a margin account.

FINRA Rule 4210 establishes margin requirements for broker-dealers and their customers. The rule sets minimum equity requirements and outlines how brokerage firms must manage margin accounts.