Complex Investment Products

Securities Fraud Attorneys for Complex Stocks and Other Investments

Investors have plenty of choices for investing their money today. Unfortunately, alternative investment products created for wealthy, experienced investors are sometimes sold to elderly or unsophisticated investors. These investments may be difficult to understand without prior training or experience. They may have significant commissions, sales charges, or fees that benefit the broker but not the investor.

Complex investment products have intricate structures and features, often designed to provide exposure to specific markets, strategies, or risk profiles. These products typically go beyond traditional investments like stocks and bonds and may involve variable annuities, non-traded investments, or structured products. While they can offer unique opportunities, it’s essential to understand their complexities and risks before investing.

Suitability is critical when it comes to complex investment products. It refers to whether a particular investment is appropriate for an individual investor based on their financial goals, risk tolerance, investment knowledge, and overall financial situation.

Are these Investments Suitable for you?

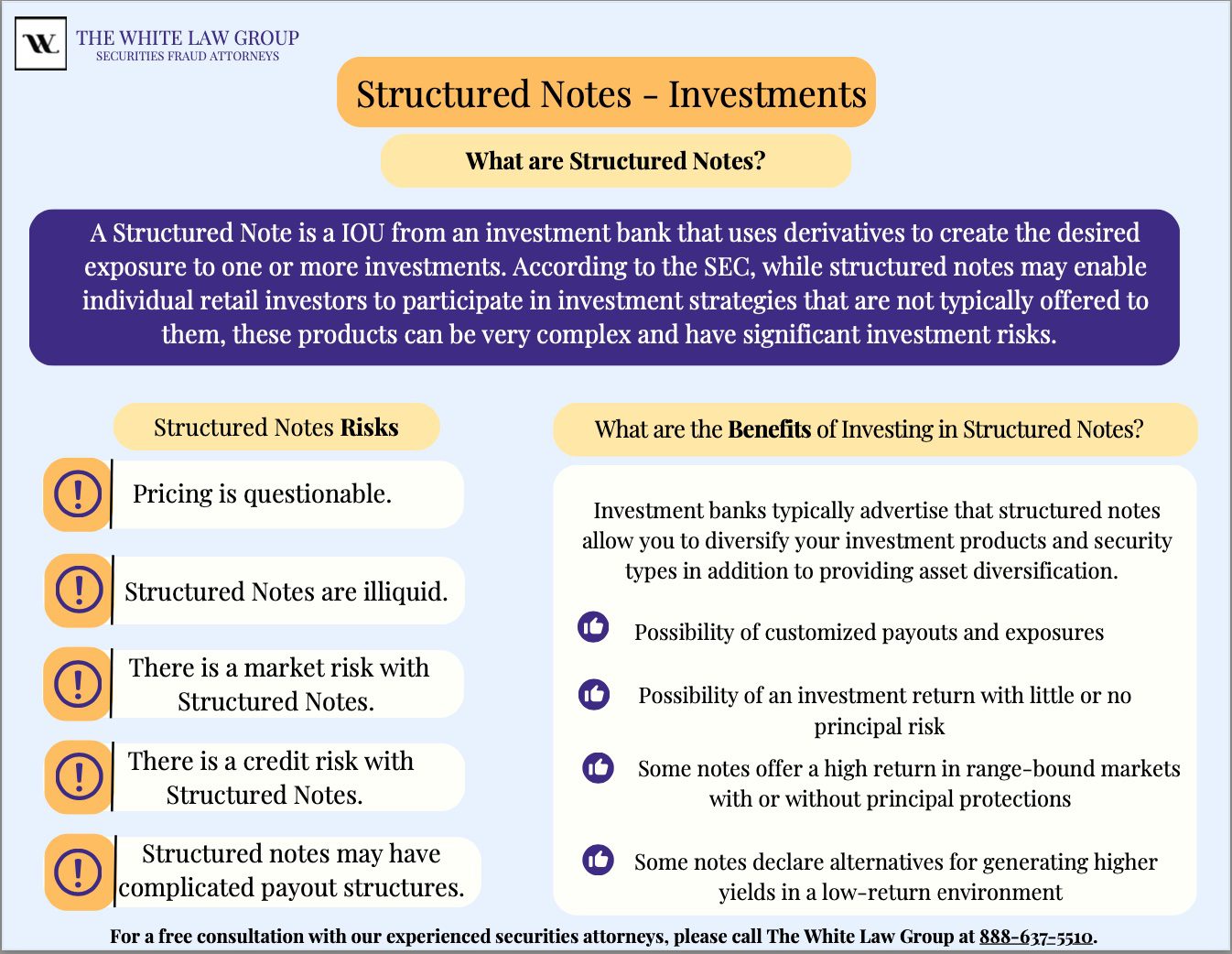

Structured products: Structured products are typically built upon financial arrangements that are more complex than securities like stocks and other well-known investment products, combining multiple underlying assets or derivatives. The intricate structures and payout mechanisms can make it challenging for investors to fully understand this complex investment product’s characteristics, potential returns, and associated risks. Lack of transparency can lead to unintended consequences and unexpected outcomes, such as significant financial losses.

Structured products: Structured products are typically built upon financial arrangements that are more complex than securities like stocks and other well-known investment products, combining multiple underlying assets or derivatives. The intricate structures and payout mechanisms can make it challenging for investors to fully understand this complex investment product’s characteristics, potential returns, and associated risks. Lack of transparency can lead to unintended consequences and unexpected outcomes, such as significant financial losses.

Investors may have limited access to information or face challenges understanding this product’s intricacies and actual value. This limited transparency can make evaluating the risks and making informed investment decisions difficult.

Alternative Investments with Limited Liquidity

Private Placement Investments

Private placement investments are considered complex, high-risk investment products due to several factors. They are typically exempt from the same level of regulatory scrutiny as investments like publicly traded securities. This reduced regulatory oversight can result in fewer investor protections and disclosure requirements. As a result, investors may have limited information about the investment, the underlying assets, and the issuing company’s financial condition. See: The Trouble with Private Placements Under Regulation D.

What truly makes private placements a complex investment product, however, is their illiquidity in comparison to stocks, meaning investors have limited opportunities to sell their holdings or access their invested capital. Unlike publicly traded securities that can be easily bought or sold on a stock exchange, private placements often involve long holding periods, lock-up periods, or restrictions on transferring ownership. Investors may face challenges in converting their investment into cash, which can result in limited flexibility and potential financial constraints.

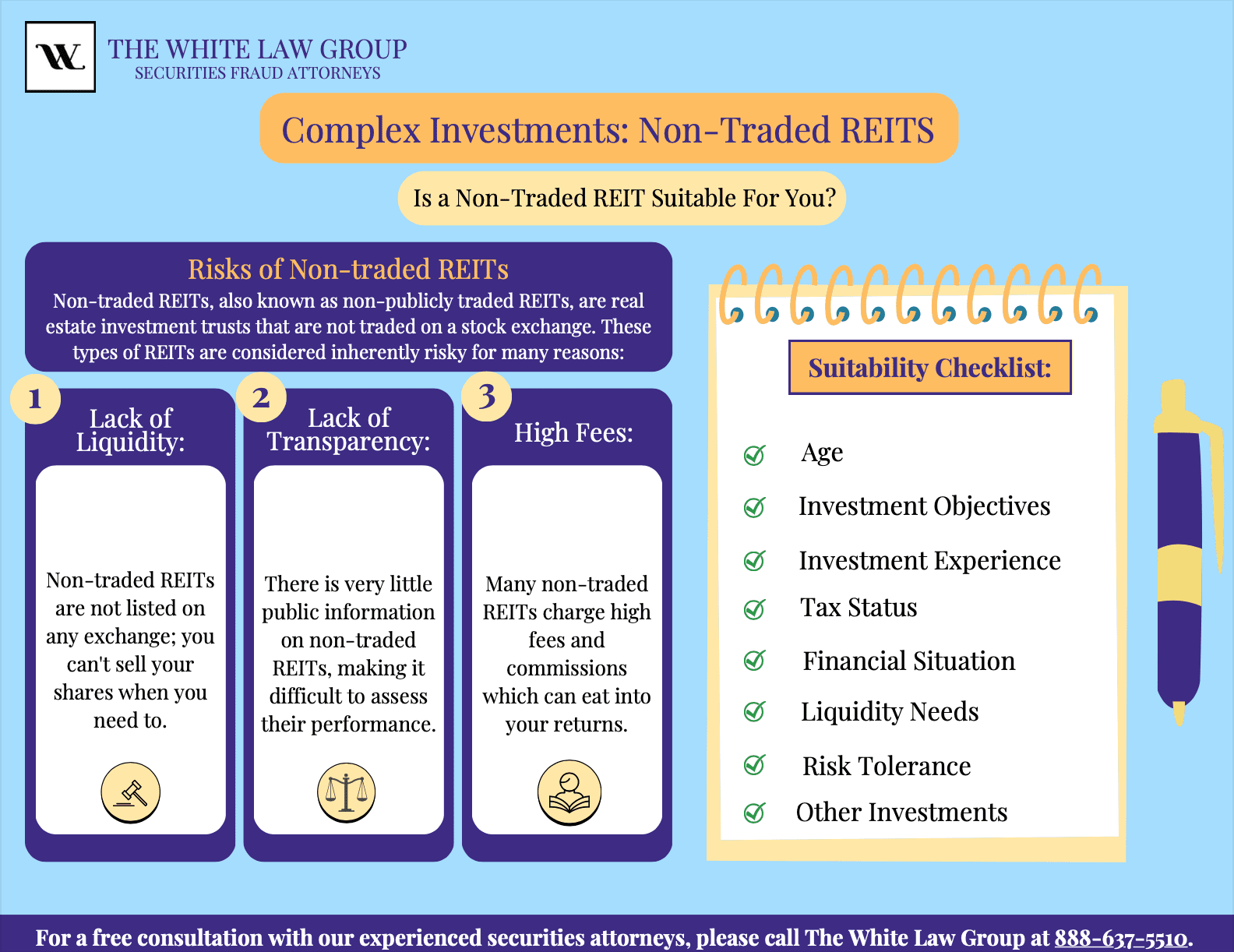

Non-traded Real estate Investment Trusts (REITs):

REITs are complex investment products, relative to other securities, that own and manage income-generating properties such as commercial buildings, residential complexes, or hospitality assets. Non-traded REITs often have higher upfront fees and ongoing expenses than publicly traded REITs. These fees include sales commissions, offering expenses, management fees, and administrative costs. High fees can erode the overall returns on the investment and potentially impact the performance of the investment.

REITs are complex investment products, relative to other securities, that own and manage income-generating properties such as commercial buildings, residential complexes, or hospitality assets. Non-traded REITs often have higher upfront fees and ongoing expenses than publicly traded REITs. These fees include sales commissions, offering expenses, management fees, and administrative costs. High fees can erode the overall returns on the investment and potentially impact the performance of the investment.

Since non-traded REITs are not traded on public exchanges, investors may face challenges obtaining current pricing information. This lack of price transparency can make REITs a more complex investment product than regular stocks because it is harder to assess the investment’s performance and potential returns accurately.

For more information, please see: Are Non-Traded REITs a Safe Bet?

Business Development Companies (BDCs):

A Business Development Company (BDC) is also considered a complex investment. BDCs are a type of investment company primarily investing in small and mid-sized private businesses. Unlike traditional BDCs that are publicly traded, non-traded BDCs do not trade on a public exchange. Similar to non-traded REITs, non-traded BDCs are complex, illiquid investment products, meaning they don’t have a market for buying and selling shares, unlike common securities. Investors typically commit their capital for an extended period, often seven to ten years or longer, and may have limited options to access their investment before the maturity of the investment. For more information, please see Business Development Companies’ BDCs – the good, the bad, and the UGLY.

BDCs typically invest in a diversified portfolio of private companies, including debt and equity securities, like stocks. These products’ underlying investment strategies and risk profiles are complex and can vary between different BDCs. Some BDCs invest in securities rated below investment grade by rating agencies. The investment grade securities below, often referred to as “junk,” have speculative characteristics concerning the issuer’s capacity to pay interest and repay principal. They may also be illiquid and difficult to value.

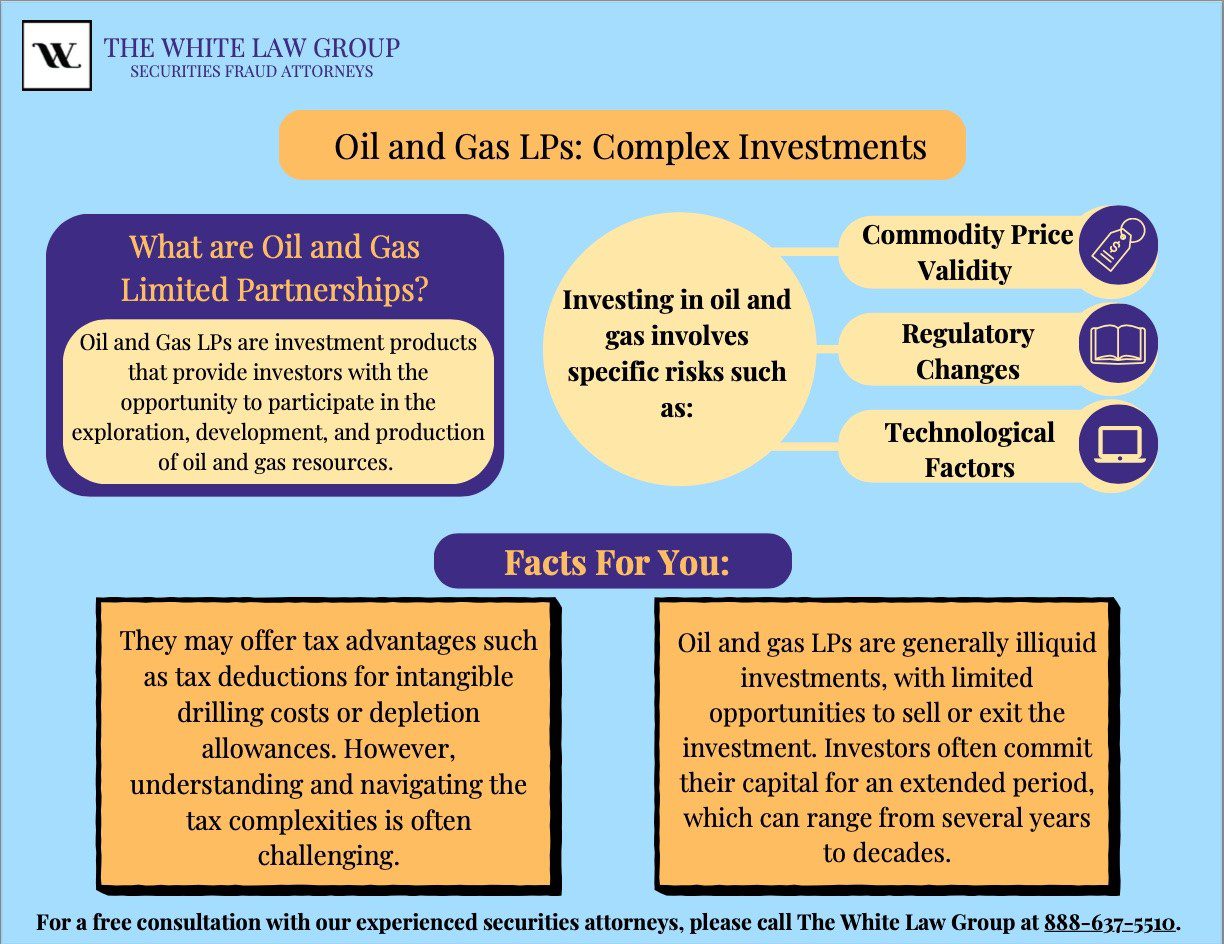

Oil and Gas Limited Partnerships (LPs):

Oil and Gas Limited Partnerships (LPs):

Oil and Gas LPs are complex investment products that allow investors to participate in the exploration, development, and production of oil and gas resources. Investing in oil and gas involves specific risks associated with the energy sector, including commodity price volatility, regulatory changes, and technological factors. These risks can significantly impact the performance and profitability of oil and gas investments.

They may offer tax advantages such as tax deductions for intangible drilling costs or depletion allowances. However, unlike common stocks and other securities, understanding and navigating the tax complexities associated with these investment products can be challenging, requiring specialized knowledge or consultation with tax professionals. Oil and gas LPs are generally illiquid investments, with limited opportunities to sell or exit the investment. Investors often commit their capital for an extended period, which can range from several years to decades, depending on the life cycle of the oil and gas project. The lack of liquidity can restrict investors’ ability to access their capital before the project’s completion.

Other High- Risk, Complex Investment Products

Variable Annuities:

Variable Annuities:

Variable annuities are considered investments for more sophisticated investors due to several factors that make them more complex than many well-known products, like stocks. For one, they have a complex structure combining insurance and investment elements. They involve a contract between the investor and an insurance company, where the investor makes premium payments, and the insurance company provides a range of investment options. The investor’s returns are tied to the performance of the underlying investment portfolio.

Variable annuities have a complex fee structure compared to other investment products, like common securities. These fees include mortality and expense charges, administrative and investment management fees, and surrender charges. These numerous fees can impact the overall return of the annuity and can be challenging for investors to understand and fully compare with other investment options.

Some unscrupulous financial advisors or brokers may encourage investors to switch from one variable annuity to another, primarily to generate additional commissions or fees for themselves. When variable annuity switching involves misrepresentation, unauthorized trading, or other fraudulent activities, it can harm investors.

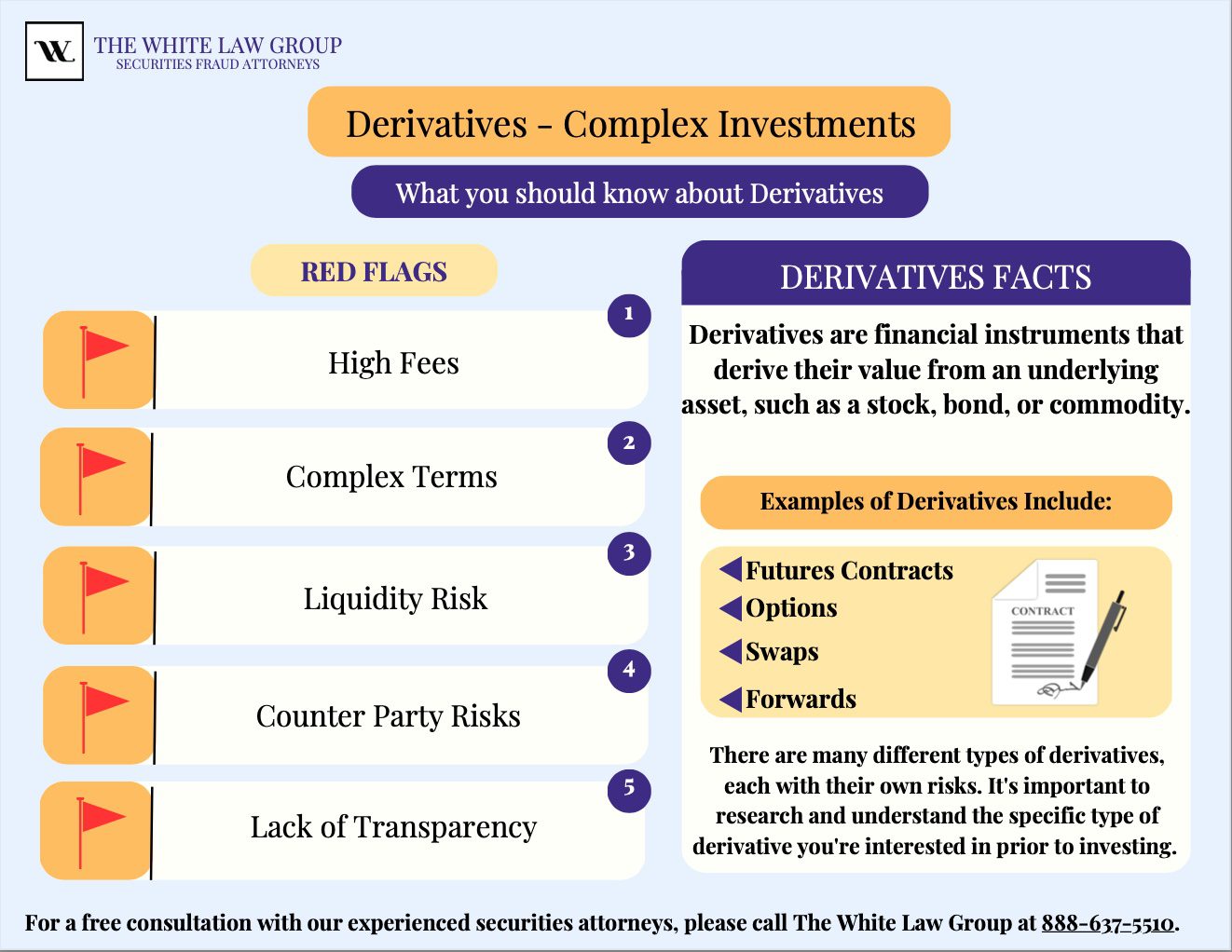

Derivatives:

Derivatives are more complex investment products than less sophisticated ones, like stocks. They consist of financial contracts whose value comes from an underlying asset, index, or benchmark. Compared to other common securities investments, derivatives are highly complex and can be used for speculation, hedging, or risk management. Examples include options, futures contracts, swaps, and forwards. Derivatives are risky because they often involve leverage and can magnify both gains and losses.

Hedge funds:

Hedge funds are investment products that pool capital from accredited investors to pursue higher returns using various strategies. These strategies can include long-short equity, arbitrage, distressed debt, or global macro investing. Hedge funds are complex investment products because they often have minimum investment requirements, limited liquidity, and charge performance-based fees. They are subject to less regulatory oversight compared to traditional investment funds.

Are Complex Investments Suitable for you?

Suitability assesses whether an investment is appropriate for an investor based on financial goals, risk tolerance, investment knowledge, and overall financial situation.

Suitability analysis becomes even more crucial when considering complex investment products such as variable annuities, structured products, or non-traded investments.

When you start working with a broker or financial advisor, you’ll fill out a suitability profile with information about your financial goals. Your broker should base his investment recommendations on this profile, but often, that is not the case. Complex investments usually require more understanding and expertise to assess their risks, benefits, and potential returns. It is essential to evaluate whether the investor has the necessary knowledge and experience to comprehend the complexities of the investment product and make informed decisions. If investors lack the required understanding, the investment may not suit them.

The suitability analysis considers whether the investor’s risk tolerance aligns with the risks associated with the complex investment. If an investor has a low-risk tolerance or cannot afford substantial risk, complex investments may not suit them.

Complex investment products have different objectives, such as capital appreciation, income generation, or hedging strategies. It is crucial to determine whether the investment can help the investor achieve their specific financial goals. Many complex assets, such as private placements or non-traded REITs and BDCs, have limited liquidity. Suitability analysis considers whether the investor has sufficient liquidity or can hold the investment for the required time frame. If an investor needs access to their funds in the short term, an illiquid complex investment product may not be suitable.

Finally, a suitability analysis considers the investor’s overall financial situation, including their income, assets, liabilities, and investment portfolio. Complex investments often require a substantial commitment of capital or have high minimum investment requirements. The analysis assesses whether investors can afford to allocate funds to a complex investment without jeopardizing their financial well-being.

FINRA Suitability Rules

The Financial Industry Regulatory Authority (FINRA), the self-regulator that oversees brokers and brokerage firms, has suitable rules and guidelines for recommending complex investment products. FINRA Rule 2111 requires that a firm or its representative have a reasonable basis to believe a recommended transaction or investment strategy involving a security is suitable for the customer. This is based on the information obtained through reasonable diligence of the firm or broker to understand the customer’s investment profile.

Brokers and advisors need to assess the suitability of these investments for each investor and provide appropriate advice regarding the risks and complexities involved.

If you believe your broker has recommended an unsuitable complex investment product and lost money, you may have recovery options. The securities attorneys at the White Law Group can assess your situation, review the relevant documentation, and determine if you have grounds for a complaint or potential legal recourse. You may be able to recover your losses through FINRA Arbitration.

FINRA Arbitration Attorneys

FINRA arbitration provides an easy and efficient forum for resolving securities disputes. It offers a streamlined process that often leads to faster resolutions than traditional court litigation. However, consulting with a firm experienced in securities law, such as The White Law Group, is essential to guide you through the arbitration process and ensure that your rights are protected.

For a free consultation with our experienced securities attorneys, please call The White Law Group at 888-637-5510.

The White Law Group, LLC is a national securities fraud, securities arbitration, investor protection, and securities regulation/compliance law firm with offices in Chicago, Illinois, and Seattle, Washington. The firm has extensive experience representing investors in unsuitable investment claims against brokerage firms and financial advisors.

For more information on The White Law Group, visit White Law Group.

Last modified: February 24, 2026